My thoughts about how crowd sentiment and overconfidence affect our expectations and publicized market prediction.

I tend to think the wisdom of the crowds is mostly a myth. Sure, it does matter for some aspects, but there are too many instances of people acting irrationally, especially when it comes to investing money and especially not recognizing the cognitive biases they face. This applies specifically to smaller groups of people prone to overconfidence and irrationality, such as participants in financial markets.

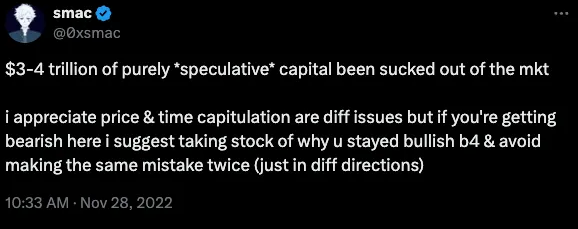

Just after the FTX collapse in November 2022, and with the QQQ’s ~30% off the ATHs, I was curious about people’s thoughts on the potential for a “soft landing.” Unsurprisingly, only 1 in 5 was fairly confident we would get one. A year later, with BTC having already doubled to ~$35k and in an undeniable uptrend, I was again curious about how people were feeling. I check polls on twitter to gauge positioning. It’s only one data point, but I find most participants do respond with what they want to happen, especially on Twitter. So, it wasn’t surprising to see only half the crowd thought a ~30% move higher was more likely than a 20% pullback, even fewer expected prices to keep rising.

At that moment, post FTX implosion, I felt confident both $45k and $60k were coming for many reasons, everyone was calling for impossible prices -lower than 10k-, crypto-haters were resurfacing and ridiculing the whole ecosystem calling it “a scam”, “only smokes”, blablabla…, crypto advertisements vanished and all the youtube and instagram griffters started looking for their next hustles!

Today, however, I have less conviction about short-term price action and weaker idea about the next 6 months. Many have been asking, “where are we in the cycle?”. This is a tricky and loaded question implying some things I’m not sure are necessarily true. Nevertheless, I will share my thoughts.

The consensus, among analysts and most respected traders on X, seems to be that we’re in the middle of the cycle. Even if this is true, it feels, it smells like a cop-out answer. This is what you say when you don’t have an opinion and want to hedge. It could be true, but I wouldn’t be writing this piece if I thought that. So, where are we in the cycle, what inning are we in, is it over or are we just getting started?

Let me start with one more tweet from November 2022.

I bring this up to illustrate that price and time are very different in the context of “this cycle.” If we look at each separately, we’re somewhere around week 70 of the bull market purely from a time perspective. I would argue this overstates the true length of this run because I can count on two hands the number of people who were actually bullish back in December 2022. If I were extremely generous, I’d say most people began to realize what was going on around late Q1/early Q2 2023. So, let’s say it’s been a bit over 12 months.

From a price perspective, we’re roughly 4.5x off the bottom on BTC and 3x off the bottom on ETH. Those who’ve been around crypto for multiple cycles feel we’re closer to the end than the beginning. Much of this is because the playbook they are/ I am accustomed to hasn’t panned out this time around. Prior crypto cycles have seen a logical flow of BTC → ETH → long-tail of crypto assets (where venture and token investments are made) as capital moves out on the risk and speculation curve, and market participants believe in new narratives. Narratives are often around fundamental shifts of what crypto enables, creating a new wave of believers who either convert for life or churn out as prices come back down once speculation subsides.

This cycle has been quite different so far, and many with prior heuristics have been slow or unwilling to adapt. To put it bluntly, that unwillingness leads to the obvious cope we read and see today! We are all human and so we can’t help but look around and judge ourselves on a relative basis. It’s not enough that we own assets that go up 3-5x when things we don’t own pump 10-20x. This is especially true if the things pumping 10-20x are things we don’t align with (..memecoins hehe). In my view, this is the crux of why many people believe we’re either in the middle or latter half of the cycle. They watched from the sidelines as assets like Solana rise from sub-$10 to over $200. They saw an explosion of memecoins doing 100-1000x’s and screamed internally about it:

- “This isn’t the right order!”

- “Why haven’t [my bags] pumped like this?!”

- “This isn’t supposed to happen yet!”

Put it simply: it is not playing out the way they/we were expecting it to. So it’s not that they/we could be wrong, but instead that the market is acting irrationally, differently. Or that cycles are compressing. Or that financial nihilism is being pushed to the extreme. I’m not ruling all of these things out, but there appears to be very little introspection going on.

To add some context, I know of many cases where juniors at other funds pitched SOL at sub $30 prices. But they were repeatedly rebuffed and dismissed. This is all to say that how people collectively experience the market as it’s going up will influence what stage they believe we’re in. Coming into this cycle, most were overexposed to the Ethereum ecosystem and underexposed to everything else. This positioning has warped the overall perception of crypto this cycle and distracted many from evaluating where we actually are.

So let’s weigh the arguments for either end of the barbell: are we closer to the early or late stages of this cycle?

- BTC ETF approved for trading 6 months ago

- ETH ETF approved for trading a week ago

I have never written about crypto market structure and why it’s a boring concept that has significant implications. This is a bit hyperbolic, but I view it as somewhat analogous to tectonic plates — gigantic, slow-moving pieces of the market’s crust. In the moment, it’s difficult to appreciate how seismic those shifts will be and what kind of impact the aftershocks will have. But imagine being in crypto for 8, 9, 10+ years and reaching this seminal moment…

- BTC ETFs are approved.

- Massive new pools of institutional capital now have legitimate access to this asset class.

- Initial inflows are dramatically stronger than consensus expectations.

But markets are forward-looking! The ETF is now approved and the flows are priced in! Markets are forward-looking, yes. But they are not omnipotent. They were literally JUST WRONG about ETF inflows. The people who understand crypto have no clue how traditional market structure works, and the people who understand traditional market structure have very little time for crypto. The ETH ETF is among us and trading. The time gap between BTC ETF & ETH’s allowed us some time for digestion, education, and post-election clarity. The structural change to crypto markets cannot be overstated.

- BTC printed 7 consecutive green monthlies staring Sep 2023

- BTC gave no opportunities for entry: 16 of 21 weeks green from mid-Oct to early-March

- BTC has effectively gone up only for the better part of a year and a half.

Prior to April, 12 of the last 15 months were green and there was a stretch from mid-October last year through early-March this year where 16 of 21 weeks were green. That is truly relentless. To be fair, very few were positioned for what we saw in the first half of 2023. Would it be shocking if we chopped around for a bit? No, I don’t think so. But markets trend and it feels like there’s still some PTSD from last cycle’s washout. I also increasingly witness that I’m having the same conversations I was having back in late 2022 / early 2023, it’s just that BTC is now ~$60k rather than $18k. They’re not completely the same, of course, but the skepticism is mostly around the idea we’ve already gone up a lot, there are no new narratives to push us higher, and that memecoins have gone ballistic already.

But none of these are real reasons to expect we should go down, in my opinion. Access to BTC ETF hasn’t even reached wirehouses, pension funds, family funds yet.. Ok, now we’re getting into some nerdy banking stuff. When I say access to the ETF hasn’t even reached wirehouses yet, I mean there’s no incentive yet for advisors to begin recommending this product to clients.

When advisors recommend trades, they are categorized as “solicited” and “unsolicited”. Solicited trades are those recommended to clients by their broker (“You should buy ABC”), whereas unsolicited trades are ones the client brings to their broker (“I want to buy XYZ”). The main distinction here is that commissions are paid only on solicited trades.

As it stands today, none of the wirehouses have allowed solicit inclusion in client portfolios for the BTC ETFs. The TLDR of this is that there is literally zero incentive for any of these advisors to recommend these products to their clients. This is just a matter of time though — all of these houses are in a holding pattern of sorts and when one goes, the rest will quickly follow.

The 13Fs continue to roll in too. An important point Eric Balchunas noted a week or two ago was that IBIT had ~60 holders reported but they only accounted for ~0.4% of total shares outstanding. The implication being “most of the bites are nibbles but there a LOT of fish”. The high-water mark so far is ~50m shares which would be about 2.5% of the total shares outstanding. Very, very early still.

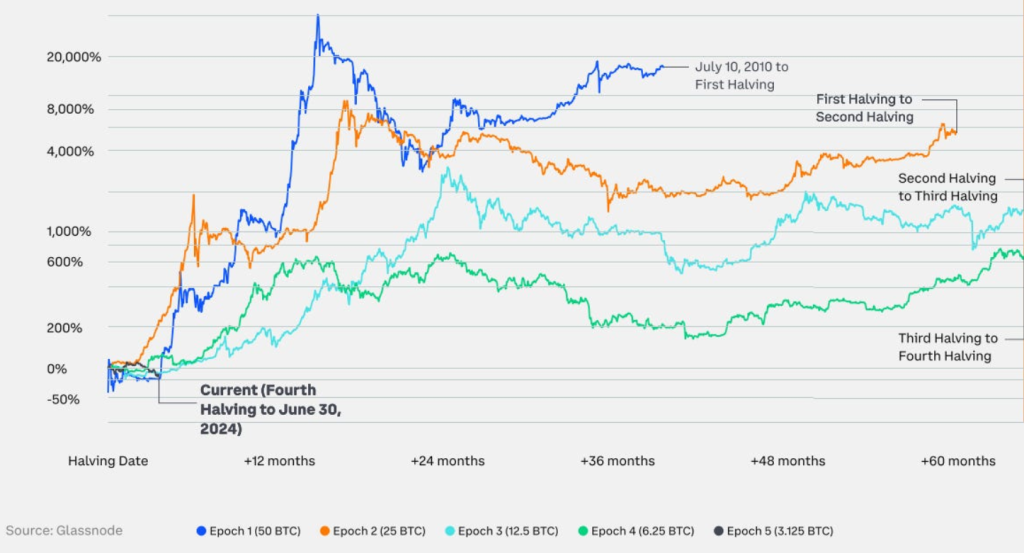

Halving in April 2024

While it’s clear to me the halving becomes less impactful as BTC continues to get bigger, it remains one of the most important components of the “cycle”. It creates this very obvious timeline of events that I think helps market participants understand where we are and what’s happening. My concern is that there’s a bit of “narrative stickiness” here where participants have incorrectly used the halving as a north star of sorts. But that feels like a problem to deal with once we cross $100k: we are not there yet!

Markets are typically forward-looking, yes and the only thing markets do better than look forward is to forget quickly. I think people are severely underestimating the type of demand that’ll come post-halving, we are in the early stage of post-halving, BTC available supply, to be traded, is already decreasing again! Remember this: following the Halvings, the price tends to trade sideways — as it is presently. However, within 12 months following the first three Halvings, the price tends to rise meaningfully (10x, 2x, 6x).

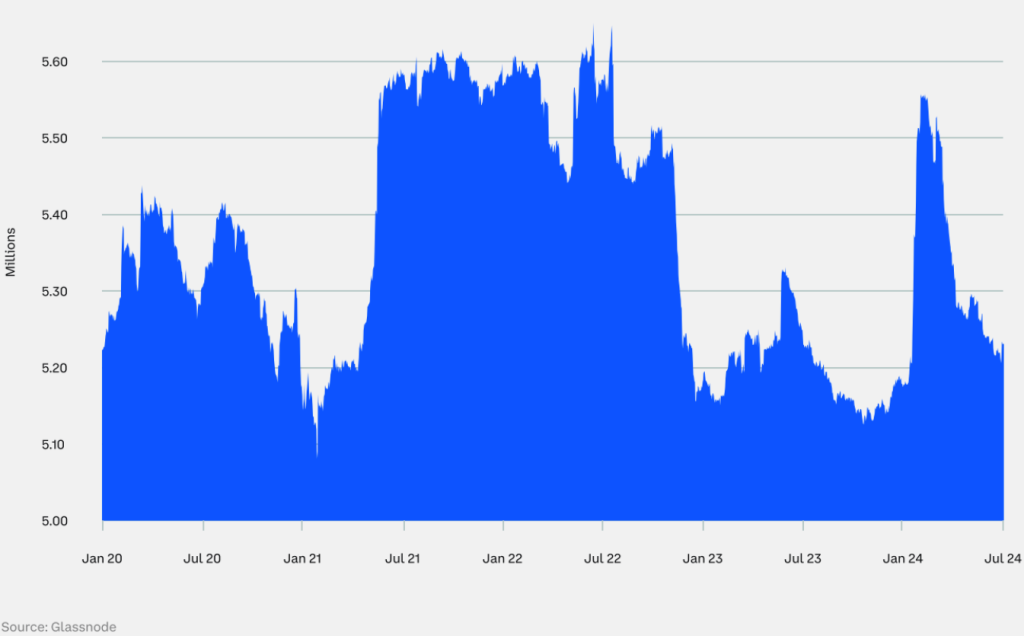

I don’t think many are thinking about this but a key element to this halving in particular is the final stage of the “sell flow” problem. Before halving, BTC’s issuance is currently 6.25/block and ETH issuance is ~2/block. Now post-halving BTC has moved to 3.125/block since April 2024. This is important to understand from the perspective of relative inflation between BTC & ETH. ETH has had deflationary supply for over 18 months now, with post-Shapella (mid-April) numbers coming in around -1.5% annualized. Even at $60k BTC with 3.125 new BTC/block, we’re looking at ~9m/day in sell pressure.

While, ETH is actually around ~7.5m/day currently, but that will grow to ~12m/day by the end of the year as more people unlock staking (more inflation). By the time the halving comes, I suspect BTC’s issuance will be far closer to ETH’s than people realize.

The term “meme” was overused in the last year and perhaps the largest meme within crypto markets right now is that “real crypto” (whatever that means) has gone nowhere this year. I think the inverse is true and this meme is just a vestige of bad portfolio management. Let’s be honest, what people mean when they say this is: “my bags haven’t gone up.”

Everything else has. There are many examples, but the most obvious being the Solana ecosystem. SOL, FTM, INJ, LDO, RNDR, and ARB, to name a few, have all performed very well since the lows of last year. People had not expected these returns because their bags didn’t move. Arweave was sub $5 for a long time and the entire industry ignored its monstrous move. Another niche example, but Proof of Stake went from ~57% of L1 supply in April to over 63% today. That’s $50 billion of crypto value.

Despite multiple market-wide drawdowns, DeFi’s TVL is up ~4-5x this year. Yes, there’s nuance, and some of that is due to more liquid staking tokens being included. But that misses the larger point, which is that the market is larger and broader than many realize. Those who were positioned properly have done well. Again, there are many examples, but you get the point. There have been huge moves, and people seem to be broadly ignoring them.

A final point I’ll make on this is that financial nihilism has been pervasive in 2023. A particularly insidious aspect of nihilism is the subconscious anchoring to ideas, heuristics, or beliefs you may not even recognize. This is usually what causes pain — the things you’re not aware of, or don’t acknowledge, because they either seem too difficult to identify or simply unimportant. Until they are.

The market (once again) has shown people it does not care about what they want to happen. The arrogance with which many have approached this cycle feels more akin to the early days of 2017 rather than 2021. Perhaps that’s why we’re so much closer to the beginning than the end this time around.